Navigating the auto insurance landscape in the United States has transformed into a highly complex financial challenge. Driven by staggering technological advancements in vehicles, rising litigation costs, and severe macroeconomic inflationary pressures, the premium rates for standard auto policies have undergone unprecedented shifts. For American drivers, securing a car insurance policy is no longer just a legal mandate to satisfy state minimums; it is a critical pillar of personal asset protection and long-term wealth preservation.

Thank you for reading this post, don't forget to subscribe!Finding the absolute “best” insurer requires moving beyond superficial television commercials and deep into the underlying financial data. A truly premier insurance carrier must balance competitive premium pricing with bulletproof financial stability, a frictionless digital claims ecosystem, and an outstanding customer satisfaction index. This definitive 2026 comparison guide breaks down the top national auto insurers in the USA, tracks changing industry metrics, and provides an actionable strategic blueprint to optimize your automotive coverage.

The 2026 Market Reality: Why Auto Insurance Costs Are Surging

Before examining individual carriers, it is vital to understand the structural economic factors currently dictating U.S. insurance premiums. The auto insurance sector is grappling with a combination of unique modern variables:

- High-Tech Repair Costs: Modern vehicles are heavily integrated with Advanced Driver Assistance Systems (ADAS), featuring complex sensors, cameras, and radar arrays built directly into bumpers and windshields. What used to be a simple $300 bumper replacement now requires thousands of dollars in technical component calibration.

- Severe Weather and Climate Risks: Comprehensive claim losses have spiked dramatically due to localized natural disasters, including severe hailstorms, flash flooding, and catastrophic wildfires across multiple states.

- Litigation Inflation: Corporate legal disputes and personal injury lawsuits are yielding significantly higher judicial settlement payouts, forcing insurance pools to adjust premiums broadly across the board to remain solvent. For a comparative look at how these massive corporate structural settle-outs operate globally, review our guide on how insurance claim settlement amounts are calculated.

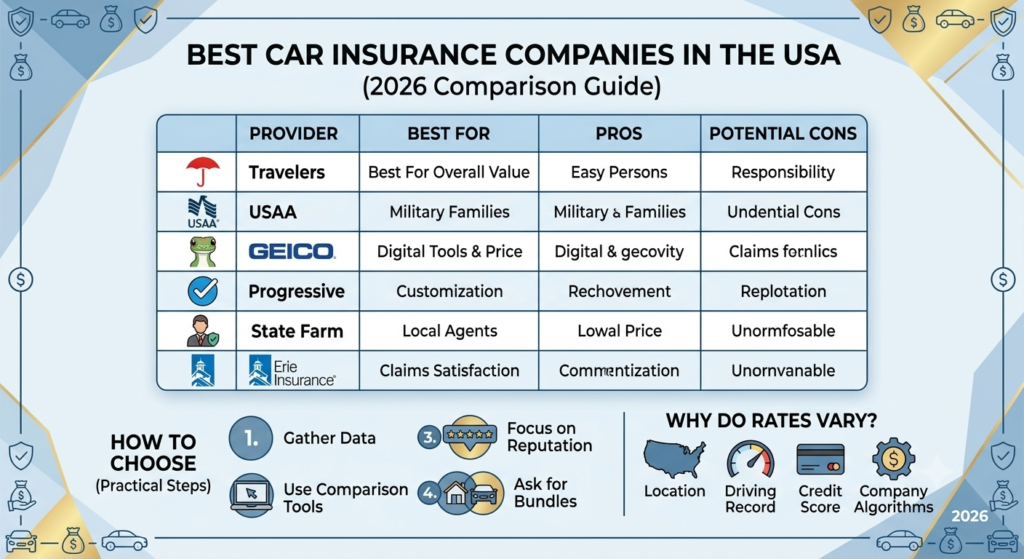

Comprehensive Analytical Matrix: Top U.S. Car Insurers Compared

To provide clear, objective clarity, we have evaluated the top auto insurance providers operating across the United States. Our ranking methodology analyzes independent data from J.D. Power customer satisfaction studies, AM Best financial strength ratings, and baseline coverage accessibility:

| Insurance Carrier | AM Best Rating | Target Market / Core Strength | Notable Policy Feature |

|---|---|---|---|

| State Farm | A++ (Superior) | Market share leader; ideal for drivers desiring localized agent relationships. | Drive Safe & Save™ telematics program offering deep discounts for safe driving. |

| Progressive | A+ (Superior) | High-risk drivers, multi-policy bundling, and tech-focused shoppers. | Name Your Price® tool coupled with highly advanced algorithmic snapshot tracking. |

| GEICO | A++ (Superior) | Budget-conscious consumers looking for seamless, automated digital management. | Extensive federal employee and military affiliation discounts across all 50 states. |

| Allstate | A+ (Superior) | Premium coverage seekers prioritizing rich feature add-ons. | Robust Claim Satisfaction Guarantee® and comprehensive accident forgiveness options. |

| USAA | A++ (Superior) | Exclusively built for military members, veterans, and immediate families. | Industry-leading customer satisfaction rankings and unmatched dividend structures. |

Deep-Dive Profiles of the Top National Carriers

State Farm: The National Giant

Capturing the largest market share in the United States, State Farm remains a dominant force. Its primary advantage is its massive network of localized, captive insurance agents. For drivers who want to sit down across a desk from a human advisor to structure a policy, State Farm is exceptional. Their financial backing is flawless, ensuring they can settle claims seamlessly even in catastrophic economic environments.

Progressive: The Telematics Innovator

Progressive is an absolute powerhouse for data-driven consumers. They were the early pioneers of usage-based insurance (UBI) through their Snapshot program, which tracks real-time driving telemetry such as hard braking, speed variations, and late-night driving. If you are an exceptionally safe, low-mileage driver, Progressive’s algorithmic pricing models can reward you with massive discounts that traditional underwriting models simply cannot match.

GEICO: The Frictionless Digital Ecosystem

A subsidiary of Berkshire Hathaway, GEICO focuses heavily on lean, direct-to-consumer digital interactions. Their mobile app is consistently rated as the best in the industry, allowing users to instantly pull up digital ID cards, request roadside assistance, add new vehicles, and file claims via automated photo uploads. GEICO keeps operational overhead low, frequently passing those savings directly to consumers through highly competitive baseline premiums.

Essential Coverage Components Every Driver Must Understand

When selecting your policy provider, the specific configuration of your coverage is just as important as the company logo on your card. A standard, comprehensive auto policy should be structured with a mix of these critical layers:

- Bodily Injury & Property Damage Liability: The foundation of any policy. This pays for the medical expenses and property repairs of other parties if you are found at fault in an accident. Always buy limits well above your state’s legal minimums to protect your personal assets from litigation.

- Collision Coverage: Pays to repair or replace your own vehicle if it is damaged in a crash with another automobile or a static object, regardless of fault.

- Comprehensive Coverage: Insures your vehicle against non-collision physical losses. This includes automotive theft, vandalism, animal strikes (such as hitting a deer), hail damage, and cracked windshields.

- Uninsured/Underinsured Motorist (UM/UIM): A vital layer that steps in if you are struck by a hit-and-run driver or a motorist who carries completely inadequate liability limits. This covers your medical bills and lost wages when the at-fault party’s pool is dry.

Understanding these distinct coverage structures is essential. If a carrier attempts to unfairly deny a legitimate comprehensive or collision claim down the line, drivers must be prepared to follow a rigorous escalation path, similar to understanding how to appeal an auto insurance claim denial effectively.

Advanced Strategies to Drive Down Your Auto Premiums

You do not have to accept soaring premium rates passively. By deploying several strategic financial adjustments, you can aggressively lower your annual insurance costs without compromising your core safety nets:

- Strategic Deductible Adjustments: Raising your comprehensive and collision deductibles from $250 to $1,000 can slash your monthly premium by up to 15% to 30%. However, ensure you maintain this deductible amount readily accessible in an emergency savings fund.

- The Power of Multi-Line Bundling: Insurance carriers aggressively reward loyalty. Placing your homeowners, renters, life, or umbrella liability insurance under the same corporate umbrella as your auto policy triggers massive multi-policy discounts across all active lines.

- Clean up Your Credit Profile: In the vast majority of U.S. states, actuarially minded insurers use credit-based insurance scores to calculate risk. Maintaining a pristine credit history directly correlates to significantly lower premium tiers.

- Audit Your Annual Mileage: If your employment structure has shifted permanently to a remote or hybrid model, notify your insurer immediately. Lower annual mileage categories reduce your overall road exposure, lowering your premium rating factor.

Consistently auditing your coverage keeps you protected from institutional mistakes, much like how evaluating how to check if you have a compensation claim works for identifying mis-sold financial products.

The Ultimate 2026 Car Insurance Acquisition Checklist

Before executing a new auto insurance contract or renewing your existing coverage, systematically complete this critical checklist:

- [ ] Verified the carrier’s financial stability rating via AM Best to ensure flawless payout capacity.

- [ ] Reviewed your state’s Department of Insurance portal to confirm the company’s local consumer complaint ratio.

- [ ] Structured liability limits to match or exceed your total personal net worth (e.g., 250/500/100 limits).

- [ ] Inquired about all applicable hidden discounts (Good Driver, Paperless, Autopay, Professional Affiliates).

- [ ] Completed a comprehensive rate comparison across at least three of the top national providers within the last 12 months.

- [ ] Confirmed that your chosen insurance carrier is fully authorized and registered by cross-referencing databases similarly to how professionals check an FCA authorised firm in the UK for regional operations.

Conclusion

There is no singular, universal “best” car insurance company in the United States; there is only the best carrier for your unique driving profile, geographic location, and financial structure. If you prioritize local human relationships and comprehensive bundling, State Farm or Allstate may lead your list. If you demand a highly streamlined digital experience at a leaner price point, GEICO or Progressive’s telematics suite will likely deliver superior value. Dedicate the time to evaluate ratings, structure your policy intelligently, and compare rates annually to keep your vehicle, your family, and your hard-earned capital entirely secure.

Disclaimer: Premium rates, specific policy features, and available discounts are highly fluid and fluctuate based on individual driving histories, credit profiling, and localized state regulations. This comparison guide is intended for general informational and educational purposes. Always obtain official, direct quotes from a licensed insurance producer or broker before executing any formal financial protection contracts.