How Long Does a Car Insurance Claim Take to Settle? (2026 State-by-State Breakdown)

Experiencing a motor vehicle collision is an inherently disruptive and stressful event. Beyond the immediate physical shock and the logistical nightmare of losing your primary mode of transportation, you are instantly forced into a complex administrative battleground: the insurance claims process. For most policyholders, the immediate, overriding question following an accident is simple yet crucial: How long does a car insurance claim take to settle? You have bills to pay, medical treatments to schedule, and a vehicle that is either sitting in a collision repair yard or completely totaled. Waiting indefinitely for financial restitution can strain your personal finances to a breaking point.

Thank you for reading this post, don't forget to subscribe!Unfortunately, there is no single, universal timeline for car insurance payouts. The speed of your financial recovery is dictated by a massive matrix of moving variables, including the complexity of the accident dynamics, whether injuries were sustained, the cooperative tendencies of the parties involved, and most importantly, statutory regulations. Every state in the U.S. enforces its own distinct “Fair Claims Settlement Practices Act,” legally dictating the exact number of days an auto insurer has to acknowledge, investigate, and either approve or deny a claim. In 2026, as supply chain backlogs continue to impact collision repair shops and digital claims adjusters rely heavily on algorithmic photo reviews, knowing your specific state laws is your greatest weapon. This definitive guide breaks down the structural mechanics of auto claim timelines, analyzes individual state mandates, and outlines advanced strategies to accelerate your insurance payout.

The Structural Architecture of a Auto Claim Timeline

To understand why some auto insurance claims wrap up in a few days while others drag on for months, you must first trace the journey of a claim through the insurance carrier’s administrative pipeline. The overall timeline is systematically divided into distinct operational phases:

The standard modern car insurance claim sequence involves a clear, linear progression of events that carriers must follow from initial lodgment to the final payout decision.

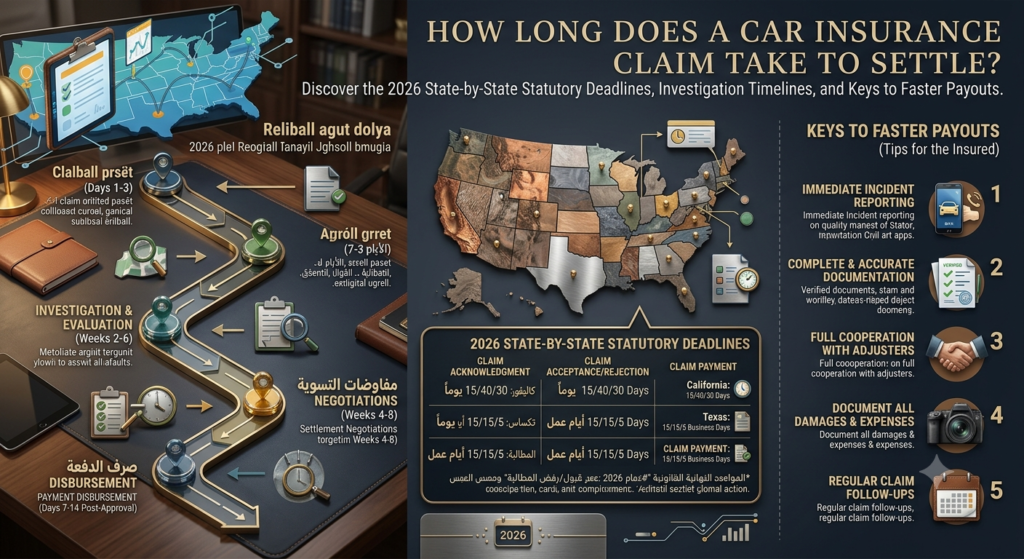

1. The Intake and Initial Acknowledgment Phase (Days 1–3)

This phase begins the moment you formally lodge your claim via your insurance provider’s mobile app, web portal, or telephonic hotline. The carrier assigns a unique claim number and routes the file to a dedicated claims adjuster. Legally, state laws require insurers to acknowledge receipt of this filing and distribute official claims forms within a set window—typically less than 15 days.

2. The Investigation and Liability Assessment Phase (Days 3–30)

This is the most volatile variable in the timeline. The adjuster must review police accident reports, interview drivers and eyewitnesses, analyze physical scene metrics, and cross-reference damage patterns. If you reside in a **fault-based insurance state**, the carrier will not issue a single dollar of payout until they definitively establish which driver holds legal liability for the impact. If liability is shared or fiercely contested by the other motorist’s insurance provider, this phase can stall for weeks.

3. The Physical Damage Evaluation and Estimation Phase (Days 5–15)

Simultaneously, the insurer must calculate the economic cost of the vehicle damage. This involves sending a field adjuster to conduct an in-person vehicle inspection, directing you to an approved direct repair program (DRP) facility, or utilizing modern AI-driven digital photo estimation tools. If the repair estimates approach or exceed the vehicle’s actual cash value (ACV)—typically a threshold of 70% to 80% depending on state law—the vehicle is officially flagged as a **Total Loss**, which alters the settlement framework entirely.

4. The Final Adjudication and Payout Phase (Days 10–45)

Once liability is determined and damages are calculated, the carrier makes a formal decision to approve or reject the claim. Upon approval, statutory state deadlines trigger, forcing the insurer to issue a electronic fund transfer (EFT) or mail a physical settlement check within a set number of business days.

2026 Comprehensive State-by-State Statutory Breakdown Matrix

The single biggest factor influencing your insurer’s sense of urgency is the statutory framework of the state where the policy is written. Insurance companies face severe regulatory penalties, licensing suspensions, and bad-faith lawsuits if they violate state-mandated timelines. Below is a comprehensive analysis of the legal deadlines across key U.S. jurisdictions:

| State | Time Limit to Acknowledge Claim | Time Limit to Decide (Approve/Deny) | Time Limit to Pay After Agreement | Maximum Legal Extension Allowance |

|---|---|---|---|---|

| California | 15 Calendar Days | 40 Calendar Days from proof of claim | 30 Calendar Days | Must provide written updates every 30 days explaining delays. |

| Texas | 15 Business Days | 15 Business Days after receiving all items | 5 Business Days | Up to 45 additional days if insurer notifies claimant of structural issues. |

| New York | 15 Business Days | 15 Business Days after proof of loss | 3 Business Days | Insurer can request extensions in writing every 90 days for complex investigations. |

| Florida | 14 Calendar Days | 60 Calendar Days for personal injury protection (PIP) | 20 Calendar Days | Strict bad-faith penalties apply if claims exceed statutory limits without cause. |

| Illinois | 15 Calendar Days | 15 Business Days from proof of loss | 30 Calendar Days | Must notify claimant if investigation takes longer than 60 days. |

| Pennsylvania | 10 Business Days | 15 Business Days after proof of loss | 30 Calendar Days | Written notification required every 45 days if investigation remains open. |

Critical Variables That Can Permanently Delay Your Settlement

While state laws outline clear baselines, certain complicating factors can legally put a claim timeline on hold. If your claim involves any of the following variables, prepare for an extended settlement timeline:

1. Severe Bodily Injuries and Ongoing Medical Treatments

If you or your passengers suffer physical injuries, **never rush into an early insurance settlement**. Once you sign a release of liability form and accept a settlement check, your claim is permanently closed. If you discover three months down the road that you require spinal surgery or extensive physical therapy, you cannot reopen the claim to demand more money. Sophisticated risk managers and legal advisors recommend waiting until you reach **Maximum Medical Improvement (MMI)**—the point at which your medical condition has stabilized and your total lifetime healthcare costs can be accurately calculated. This can add months or even years to the final settlement date, but it is the only way to protect your financial safety.

2. Complex, Disputed Fault Dynamics

In a standard rear-end collision, establishing fault takes less than 24 hours. However, in multi-vehicle pileups or lane-merging accidents where both drivers present completely contradictory stories, the claims process slows significantly. If no independent eyewitnesses or dashcam videos exist, the insurance companies will enter a formal dispute resolution process known as **Arbitration**. This third-party review adds 30 to 90 days to the timeline as insurers fight over percentage allocations of fault.

3. Total Loss Structural Valuations

When a vehicle is totaled, the adjuster must calculate its Actual Cash Value using proprietary valuation databases (like CCC Intelligent Solutions). This process is notorious for generating friction, as the insurer’s initial valuation is frequently lower than the owner’s expectations or the outstanding balance on their auto loan. Negotiating a fair total loss payout requires pulling localized market comparables and invoking the policy’s **Appraisal Clause**, which routinely adds 2 to 4 weeks to the settlement process. For an analytical breakdown of how these intricate claims valuations and insurance pay structures operate, look directly into our comprehensive guide on how insurance claim settlement amounts are calculated.

The Legal Recourse: What to Do When a Carrier Violates State Timelines

If your auto insurance carrier blows past their state-mandated deadlines, stops responding to your digital communications, or leaves your claim in an indefinite status without providing a written explanation, they may be guilty of **Statutory Bad Faith**.

Insurance companies are legally bound by a covenant of good faith and fair dealing. When they violate this covenant, you have the right to escalate the matter beyond their internal customer service management tiers:

- File a Formal Complaint with the State Department of Insurance (DOI): Every state maintains an insurance regulatory commissioner. Filing an official complaint triggers an administrative investigation into the carrier’s claims practices, forcing them to assign senior compliance managers to your file to avoid regulatory fines.

- Execute a Formal Appeal Strategy: If the carrier uses the extended delay to gather evidence for a bad-faith denial of coverage, your risk mitigation team must act. You can deploy tactical appeal protocols, similar to mastering how to appeal an auto insurance claim denial, to legally force the carrier to re-evaluate your policy standing and expedite your payout.

Advanced Blueprint: Tactical Strategies to Accelerate Your Insurance Payout

You do not have to sit back and wait for a slow adjuster to handle your file. By executing a highly disciplined, proactive operational approach, you can cut your settlement timeline by 50%:

Leverage the Power of Comprehensive Digital Documentation

Do not wait for the adjuster to request documentation. Within 48 hours of the accident, upload a clean digital package containing high-resolution scene photographs, dashcam footage, a copy of the official police report exchange sheet, and organized medical treatment receipts directly into the carrier’s web portal. Delivering an unassailable, ready-to-adjudicate file leaves the adjuster with zero excuses to delay your review.

Utilize Your Own Collision Coverage via Subrogation

If the at-fault driver’s insurance carrier is stalling, dragging out their investigation, or refusing to return calls, stop wasting time dealing with them. If your personal policy includes **Collision Coverage**, file the claim through your own insurer. Your company will pay to repair your vehicle or cut you a total loss check immediately (minus your deductible). Your insurer will then deploy their internal legal assets to collect the funds from the at-fault driver’s carrier via a formal process known as **Subrogation**. Once subrogation concludes, your insurer will refund your out-of-pocket deductible.

When dealing with international commercial vehicle operations or structured corporate transit lines, validating the formal operational licensing and regulatory compliance of all involved logistics and insurance entities is standard risk protocol. Ensure your legal advisors understand exactly how to check an FCA authorised firm in the UK if your claims pathways intersect with global corporate underwriting groups.

The Ultimate Car Insurance Claim Acceleration Checklist

To guarantee that your auto claim moves through the carrier’s pipeline at the absolute fastest legal velocity, systematically cross-reference and execute every item on this operational checklist:

- [ ] Reported the motor vehicle collision to your insurance provider within the initial 24-hour window following the incident.

- [ ] Secured the official police report number and verified that the investigating department has uploaded the finalized report.

- [ ] Photographed all physical vehicular damage, environmental factors, skid marks, traffic signals, and the insurance cards of all involved motorists.

- [ ] Looked up your state’s specific statutory “Time Limit to Decide” and noted the exact calendar deadline on your tracking log.

- [ ] Maintained a meticulous communication diary, logging the date, time, employee ID, and exact statements made by every adjuster during phone calls.

- [ ] Verified whether your policy includes automated rental car reimbursement to maintain your personal mobility during extended repair timelines.

- [ ] Established a clear internal baseline to cross-check your potential legal entitlements, mirroring the proactive measures used when researching how to check if you have a compensation claim for unresolved vehicle losses.

Conclusion

The time it takes to settle a car insurance claim is not a complete mystery; it is a timeline heavily governed by the laws of your state and the precision of your documentation. While simple property damage claims can resolve in a matter of weeks, complex multi-vehicle disputes and severe bodily injury files require patience to ensure you secure the full financial recovery you are legally owed. By understanding your state’s fair claims practices, building an unassailable digital evidence package, and holding your adjuster accountable to statutory deadlines, you can successfully navigate the insurance maze. Stay proactive, document every interaction, and use the full weight of regulatory law to bring your claim to a fast, fair, and successful settlement.

Disclaimer: This comprehensive state-by-state claims analysis guide is provided strictly for educational and general informational purposes. Individual auto insurance policies, carrier underwriting guidelines, and state insurance regulations are highly dynamic and subject to frequent legislative and judicial amendments. This content does not constitute formal legal or professional financial risk management advice. All policyholders must consult with a fully licensed independent insurance broker or a specialized personal injury attorney to evaluate the unique metrics governing their specific claim timeline.